When planning to buy a car, many people get confused between a car loan and a personal loan. Both options can help you purchase a vehicle, but they differ in interest rates, eligibility, repayment terms, and overall cost.

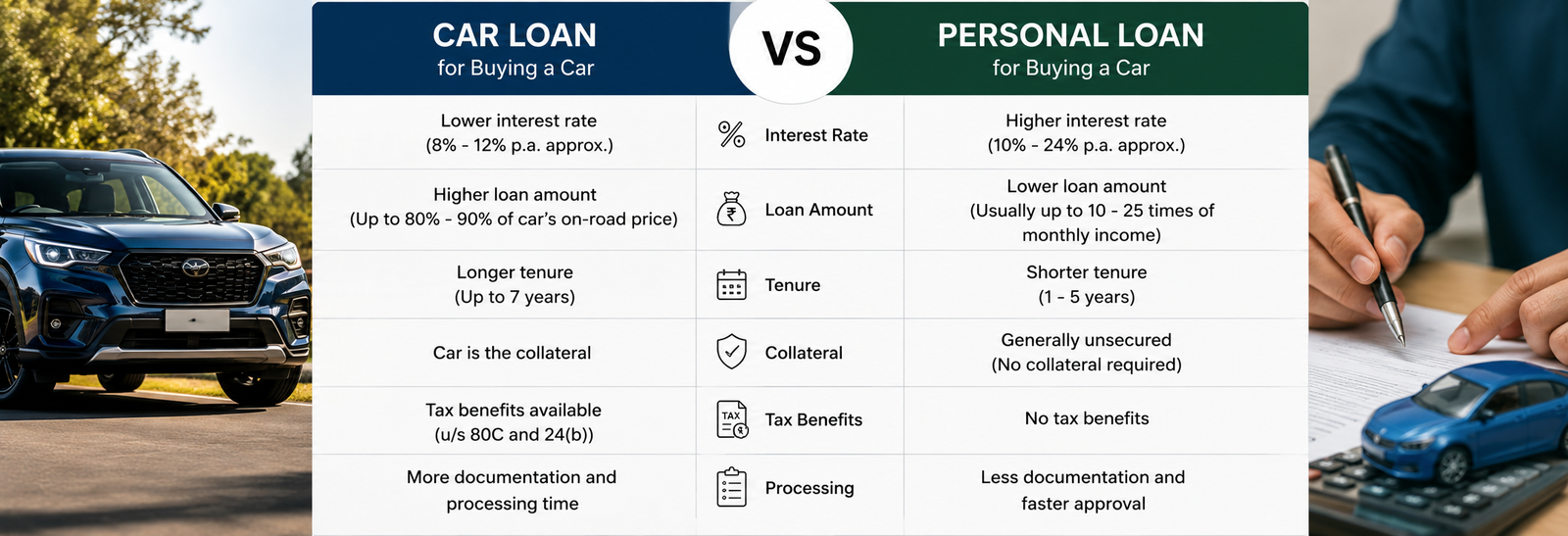

A car loan is a secured loan specifically designed for purchasing a vehicle. The car itself acts as collateral until the loan is fully repaid, making it a safer option for lenders.

A personal loan is an unsecured loan that can be used for any purpose, including buying a car. It does not require collateral, but usually comes with higher interest rates.

Car loans generally offer lower interest rates because they are secured against the vehicle. Personal loans have higher interest rates due to the lack of security.

Car loans may require additional documentation related to the vehicle and down payment. Personal loans are quicker to process but depend heavily on your credit score and income stability.

Car loans usually offer higher loan amounts based on the vehicle’s value and come with longer repayment tenure. Personal loans may have shorter repayment periods and are limited by your income eligibility.

Car loans usually require a down payment from the buyer. Personal loans do not require any down payment since the loan is not linked to the vehicle price.

In a car loan, the vehicle remains hypothecated to the lender until full repayment. In a personal loan, the car is fully owned by you from the start.

If you want lower interest rates and higher loan amounts, a car loan is usually the better option. If you need quick approval and flexibility, a personal loan can be considered, though it may cost more.

Both car loans and personal loans can help you buy a vehicle, but the right choice depends on your financial situation, credit score, and repayment ability. Always compare options before making a decision.