When it comes to financing, both EDI loans and personal loans serve different purposes. Understanding their key differences can help you choose the right option based on your financial needs.

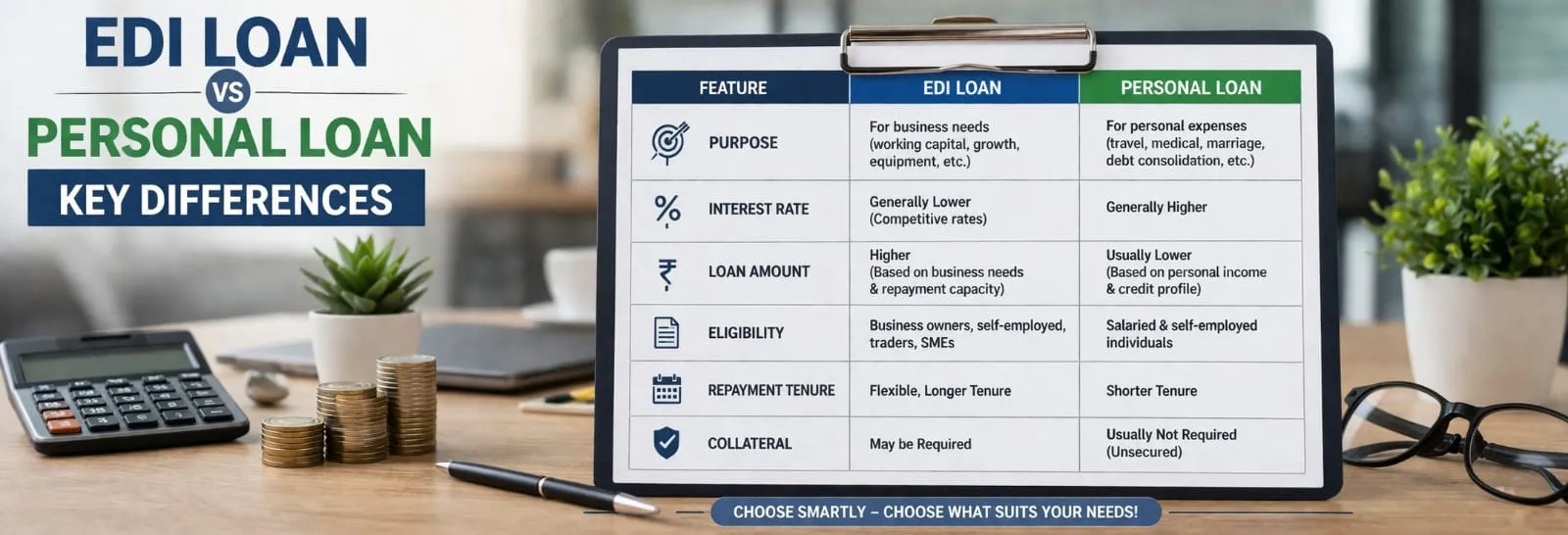

EDI loans are specifically designed for business growth, expansion, and working capital needs. Personal loans, on the other hand, can be used for any personal expenses such as travel, medical emergencies, or weddings.

EDI loans are usually business-oriented and may be secured or unsecured. Personal loans are typically unsecured and do not require collateral.

EDI loans often come with lower interest rates compared to personal loans, especially if supported by government schemes or collateral.

EDI loans generally offer higher loan amounts depending on business needs, while personal loans have comparatively lower limits based on income.

EDI loans may offer longer repayment tenures suitable for business growth. Personal loans usually have shorter tenures ranging from 1 to 5 years.

EDI loans require business-related documents, financial statements, and proof of business operations. Personal loans focus more on individual income and credit score.

EDI loans involve more detailed documentation such as GST returns, business proof, and financial records. Personal loans require minimal documents like KYC and income proof.

Personal loans are usually approved faster due to minimal documentation. EDI loans may take longer due to business evaluation.

Choose an EDI loan for business-related expenses and expansion. Opt for a personal loan for short-term personal financial needs.

Both EDI loans and personal loans have their own advantages. The right choice depends on your purpose, financial profile, and repayment capacity. Always compare options before making a decision.