Payday loans are short-term financial solutions designed to help individuals manage urgent expenses before their next salary arrives. Before applying, it is important to understand how payday loan interest rates work, what charges are involved, and how repayment affects your finances.

A payday loan is a short-term unsecured loan generally taken to handle emergency expenses such as medical bills, utility payments, rent, or urgent personal needs. These loans are usually processed quickly with minimal documentation. You can explore quick funding options through our Payday Loan services.

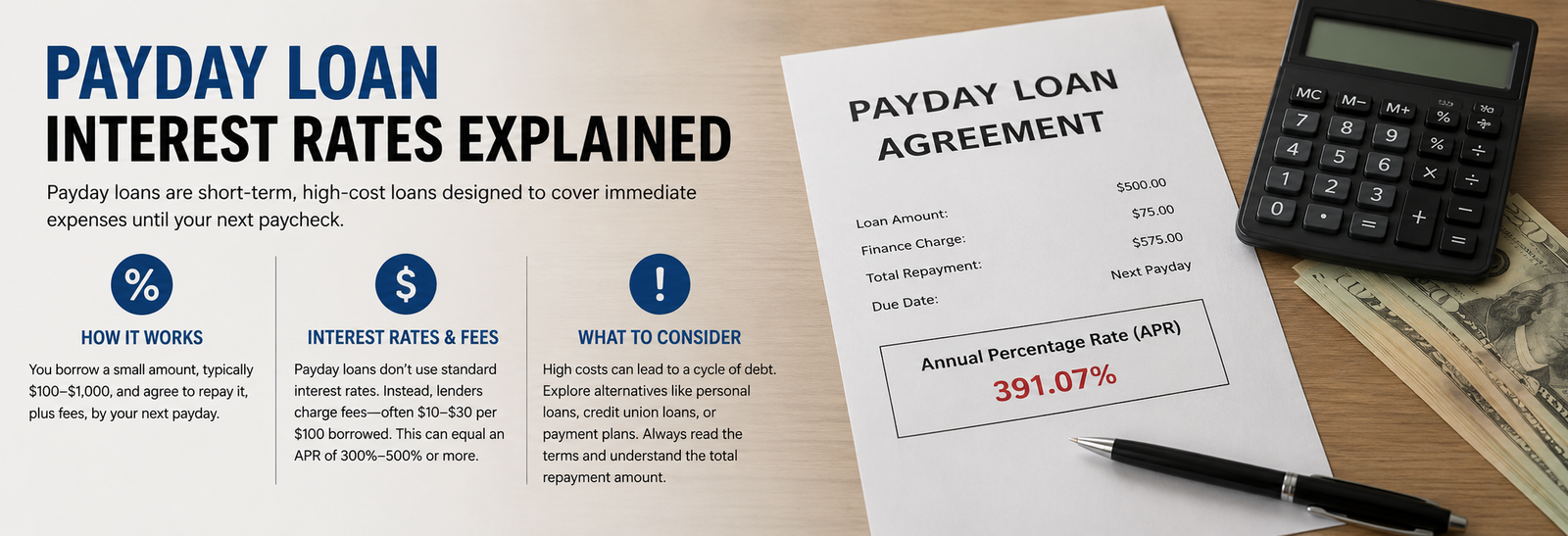

Payday loan interest rates are generally higher than traditional loans because they are short-term and unsecured. The lender calculates interest based on the loan amount, repayment duration, and borrower profile.

Several factors influence payday loan interest rates, including your monthly income, repayment capacity, employment status, credit history, and loan tenure. Maintaining a stable income and good repayment record may help you get better loan terms.

Along with interest rates, borrowers should also review processing fees, late payment charges, foreclosure fees, and penalty charges. Understanding the total repayment amount helps avoid financial stress later.

Payday loans are meant for short-term emergencies, while Personal Loans are usually available for larger amounts and longer repayment periods. Personal loans may offer lower interest rates depending on eligibility and credit profile.

You may consider a payday loan when facing urgent expenses such as emergency travel, medical bills, sudden repairs, or temporary cash shortages before salary credit.

Most lenders require applicants to be salaried or self-employed individuals with a regular source of income, valid identity proof, bank statements, and minimum age eligibility.

Common documents include Aadhaar Card, PAN Card, salary slips or income proof, bank statements, and address proof for loan verification.

Borrow only the required amount, repay on time, avoid multiple short-term loans simultaneously, and compare lenders before applying to manage your repayment efficiently.

If you require a larger amount for business or property-related needs, you can also explore options like Business Loan, Loan Against Property, or specialized funding solutions like EDI Loan.

Payday loans can be useful during financial emergencies when managed responsibly. Understanding payday loan interest rates, repayment terms, and additional charges helps borrowers make informed financial decisions and avoid unnecessary debt burden.