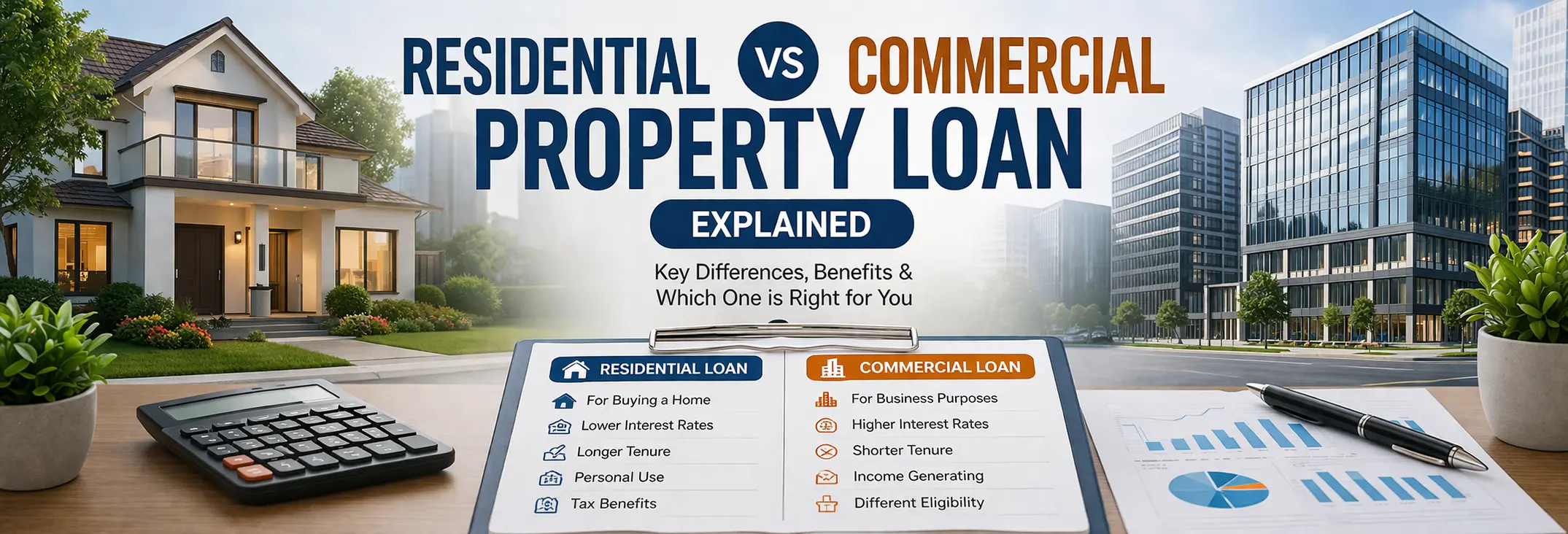

Property loans are commonly used to finance the purchase or mortgage of real estate. These loans are generally divided into two categories: residential property loans and commercial property loans. While both help borrowers secure funds using property, they differ in purpose, loan terms, interest rates, and eligibility requirements.

1. What is a Residential Property Loan?

A residential property loan is designed for properties used for living purposes such as houses, apartments, or residential plots. These loans are commonly taken by individuals who want to buy, construct, or renovate a home.

2. What is a Commercial Property Loan?

A commercial property loan is used to finance properties meant for business purposes. This includes offices, retail shops, warehouses, and commercial buildings. Businesses and investors often use these loans to expand their operations.

3. Purpose of the Loan

The main difference between these two loans is their purpose. Residential property loans are used for housing needs, while commercial property loans are intended for business or investment purposes.

4. Interest Rates

Residential property loans usually have lower interest rates because they are considered less risky by lenders. Commercial property loans generally have slightly higher interest rates due to the business-related risk involved.

5. Loan Amount

The loan amount for residential properties depends on the property value and borrowerÔÇÖs income. Commercial property loans may offer higher amounts depending on the business value and commercial property worth.

6. Repayment Tenure

Residential property loans usually have longer repayment tenures that can extend up to 20ÔÇô30 years. Commercial property loans often come with shorter repayment periods compared to residential loans.

7. Eligibility Criteria

For residential property loans, lenders mainly evaluate the borrowerÔÇÖs income, employment stability, and credit score. In commercial property loans, lenders may also consider business performance, financial records, and profitability.

8. Risk Factors

Residential properties generally carry lower risk for lenders because housing demand is consistent. Commercial properties may involve higher risk since business income can fluctuate depending on market conditions.

9. Tax Benefits

Residential property loans often provide tax benefits on principal repayment and interest under applicable tax laws. Commercial property loans may offer fewer tax benefits but can sometimes be claimed as business expenses.

10. Which Loan Should You Choose?

The choice between a residential and commercial property loan depends on your purpose. If you need financing to buy or build a home, a residential property loan is suitable. If you are planning to purchase property for business use or investment, a commercial property loan may be the right option.

Conclusion

Both residential and commercial property loans serve different financial needs. Understanding the differences in interest rates, eligibility, loan tenure, and risk factors can help you make the right decision. Always compare lenders and loan terms before applying for a property loan.